For all the hype, applying AI to investment still has a few serious problems

Artificial intelligence and machine learning are the buzzwords in automated investment. But for all the hype, applying AI to investment still has its problems.

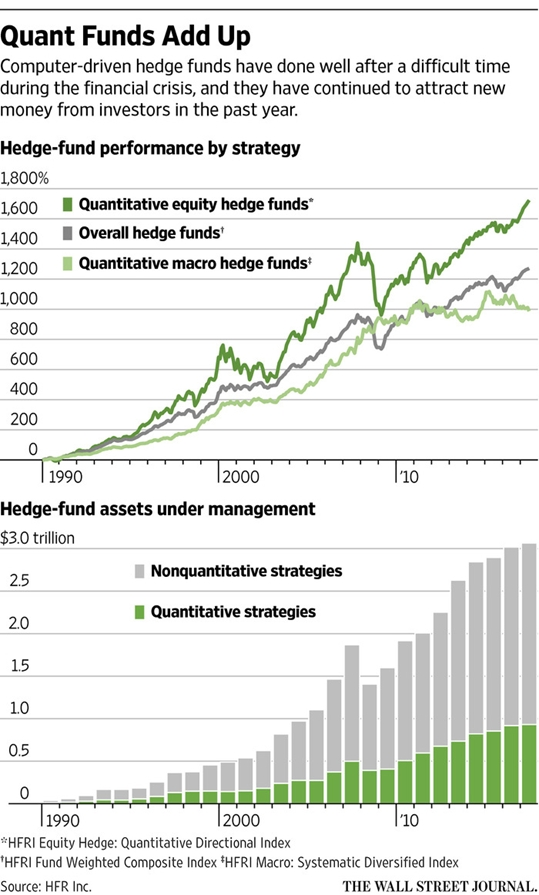

Ten years ago, computer-driven traders pulled the plug after their algorithms ran amok, leading to billions in losses and the eventual closure of Goldman Sachs ’s flagship quantitative fund.

A decade on, artificial intelligence and machine learning are the buzzwords in automated investment. But for all the hype, applying AI to investment has three serious problems: it works too well, it is often impossible to understand, and it only knows about recent history. Worse, it will be self-defeating if it proves popular, as algorithms face off against each other in the market.

Machine-learning systems are now really good at spotting patterns. Unfortunately, computers are just too good, and frequently find patterns that aren’t really there.Michael Kollo, chief strategist at Axa IM Rosenberg Equities, points to the neural network—a type of AI loosely modeled on brains—developed by three University of Washington researchers to distinguish between pictures of wolves and dogs by associating wolves with snow.

“It can easily identify something of an intransigent nature and learn one rule from it,” he says. Train an AI on the last 35 years of markets, and it might well develop a single simple rule: buy bonds. With 10-year Treasury yields down from 13.7% in July 1982 to 2.31% on Monday, it worked beautifully in hindsight—but yields can’t possibly fall that much again in the next 35 years.

In the industry, spotting patterns that don’t repeat is known as “overfitting”—picking up on the irrelevant snow in the picture of a wolf, or chance patterns in past stock prices that bear no relation to the future.

David Harding, founder of hedge fund Winton Group, says finding ways to avoid such fake patterns is at the core of computer-driven investment.

“Avoiding overfitting is a state of mind,” he says. “It’s the same thing as avoiding wishful thinking.”

Anthony Ledford, chief scientist at quant fund Man AHL, says more advanced machine learning systems sometimes prove less useful, too. “The more complicated your model the better it is at explaining the data you use for the training and the less good it is about explaining the data in the future,” he says. A model needs to accept that much that goes on in markets is meaningless noise, and try to pick out broader signals, even if it leaves some moves in past data unexplained.

Many quantitative investors try to avoid overfitting by insisting that any rule they adopt should have an economic or behavioral rationale. If the computer finds that every third Wednesday when it rains in Kansas the stocks of oil companies listed in Paris go up, betting on it happening in future would be no more than a leap of faith.

Unfortunately, explaining why a system with thousands of inputs made a decision can be all but impossible—and is such a serious problem that America’s defense research agency is financing a program to try to produce AI which explains itself.

The lack of transparency means the most advanced systems tend to be run on a tentative basis, with only a small amount of money or with human oversight of the recommendations.

Charles Ellis is typical. He joined Mediolanum Asset Management in Dublin in November to develop machine learning systems, with the first up and running providing recommendations for sectors. Given 20 years of data on 1,500 variables related to U.S. stocks, it uses a machine learning system known as random forest regression to try to avoid overfitting, and early results are good, he says. It is being used only for a small part of the $20 billion portfolio, with final decisions still made by fund managers. A second system designed to try to predict the economic cycle is currently bullish.

The drawback of the random forest method is that it is hard to understand why the computer reached any particular decision.

“It’s a little bit of a black box in that you don’t know why [the input]’s having that effect,” he says.

Mr. Kollo says it will be hard to avoid shutting down a system when it loses money if it isn’t properly understood.

“All things go wrong eventually, every algorithm has a bad day,” he says. “The difference between those that survive and don’t is those that can explain what they do.”

Some investors don’t care about the lack of transparency. Jeffrey Tarrant, whose Protégé Partners invests in hedge funds, says it “doesn’t bother me at all.” He’s invested in six funds which use AI methods—typically combined with unusual data sources—and whose managers come from nonstandard backgrounds. He estimates there are 75 funds which say they use AI, but thinks only 25 really do.

Investors who have long managed money using computers are scornful of the latest fashion for AI.

“Thirty years of being treated like an idiot for saying you can manage money with computers, and now they come along and say you can manage money with computers,” scoffs Mr. Harding at Winton.

His application of a form of machine learning to moving averages of futures prices helped him become a billionaire. His team treats machine learning as just another statistical technique to spot market anomalies.

Sushil Wadhwani used machine learning when head of systems trading at hedge fund Tudor two decades ago, and now runs his own automated fund using machine learning—but overrides the systems occasionally. In 2008 he turned off the European bond analysis because it had learned that spreads between the best and worst eurozone bonds didn’t depend on economic fundamentals, after years of evidence. As the banking system imploded, he knew this no longer applied.

“It would be very difficult for a machine to learn that unless it knew it should be looking at the 1930s,” he says.

High-frequency systems may get enough examples of changing trading regimes to run on their own, but can’t deploy much capital. Applying machine learning to longer-term investment is tricky when many of the new data sets being deployed only go back a decade or two. Computers with no knowledge of history are doomed to repeat its mistakes.