This article offers a survey of theoretical research on disclosure and the cost of capital. We summarize the current state of the literature and discuss the channels through which information affects the cost of capital. After giving an overview of asset pricing theory, we examine the rationale for an accounting risk factor or an ex-ante effect of information on the cost of capital. Then, we discuss the role of voluntary disclosure, heterogenous beliefs, investor base, liquidity shocks, earnings management, and agency problems as determinants of the cost of capital. Linkages between productive decisions and the cost of capital, and their implication for investor welfare, are also examined.

19 junho 2016

Divulgação e custo do capital: uma revisão da literatura

Resumo:

This article offers a survey of theoretical research on disclosure and the cost of capital. We summarize the current state of the literature and discuss the channels through which information affects the cost of capital. After giving an overview of asset pricing theory, we examine the rationale for an accounting risk factor or an ex-ante effect of information on the cost of capital. Then, we discuss the role of voluntary disclosure, heterogenous beliefs, investor base, liquidity shocks, earnings management, and agency problems as determinants of the cost of capital. Linkages between productive decisions and the cost of capital, and their implication for investor welfare, are also examined.

This article offers a survey of theoretical research on disclosure and the cost of capital. We summarize the current state of the literature and discuss the channels through which information affects the cost of capital. After giving an overview of asset pricing theory, we examine the rationale for an accounting risk factor or an ex-ante effect of information on the cost of capital. Then, we discuss the role of voluntary disclosure, heterogenous beliefs, investor base, liquidity shocks, earnings management, and agency problems as determinants of the cost of capital. Linkages between productive decisions and the cost of capital, and their implication for investor welfare, are also examined.

18 junho 2016

Fato da Semana: o RJ decreta estado de calamidade

Fato: O estado do RJ decreta Estado de Calamidade

Data: 17 de junho de 2016

Fonte: Imprensa

Precedentes

02/out/09 - O Rio de Janeiro é escolhido como sede dos jogos olímpicos de 2016. O governador responsável era Sérgio Cabral Filho.

2015 - A redução do preço do petróleo diminui a transferência de recursos dos royalties do produto para o estado. Ao mesmo tempo, a maior recessão dos últimos tempos diminui a arrecadação de impostos. Para complicar, os custos não previstos, Zika vírus, doping dos atletas russos e atrasos nas obras podem prejudicar os jogos.

2016 - A crise de agrava.

17/06/2016 - O estado decreta calamidade para obter recursos do governo federal, que também não pode ajudar substancialmente.

18/06/2016 - O governo empresta quase 3 bilhões para o estado.

Notícia boa para contabilidade? Horrível. Nos últimos meses diversas unidades da federação tiveram que conviver com atrasos nos pagamentos (inclusive de funcionários) e malabarismos para fechar as contas. A LRF parece que não ajuda; a contabilidade pública é arcaica, focado no caixa, não consegue evidenciar claramente a situação de cada ente. E não existe uma solução à vista.

Desdobramentos: Obras não serão concluídas no prazo, mas a imprensa provavelmente irá transmitir uma imagem de felicidade, emoção e brilho. Mas os responsáveis pela decisão de fazer um evento como este sem o respaldo financeiro não serão punidos.

Mas a semana só teve isto? A provável mudança no Iasb e a discussão sobre os números não GAAP são eventos interessantes.

Data: 17 de junho de 2016

Fonte: Imprensa

Precedentes

02/out/09 - O Rio de Janeiro é escolhido como sede dos jogos olímpicos de 2016. O governador responsável era Sérgio Cabral Filho.

2015 - A redução do preço do petróleo diminui a transferência de recursos dos royalties do produto para o estado. Ao mesmo tempo, a maior recessão dos últimos tempos diminui a arrecadação de impostos. Para complicar, os custos não previstos, Zika vírus, doping dos atletas russos e atrasos nas obras podem prejudicar os jogos.

2016 - A crise de agrava.

17/06/2016 - O estado decreta calamidade para obter recursos do governo federal, que também não pode ajudar substancialmente.

18/06/2016 - O governo empresta quase 3 bilhões para o estado.

Notícia boa para contabilidade? Horrível. Nos últimos meses diversas unidades da federação tiveram que conviver com atrasos nos pagamentos (inclusive de funcionários) e malabarismos para fechar as contas. A LRF parece que não ajuda; a contabilidade pública é arcaica, focado no caixa, não consegue evidenciar claramente a situação de cada ente. E não existe uma solução à vista.

Desdobramentos: Obras não serão concluídas no prazo, mas a imprensa provavelmente irá transmitir uma imagem de felicidade, emoção e brilho. Mas os responsáveis pela decisão de fazer um evento como este sem o respaldo financeiro não serão punidos.

Mas a semana só teve isto? A provável mudança no Iasb e a discussão sobre os números não GAAP são eventos interessantes.

17 junho 2016

Links

Excesso de plástica de Meg Ryan e a batalha da idade (foto)

Por cinquenta anos, vendeu a informação da hora correta

Menino de 12 anos fala da ligação entre vacina e autismo (vídeo)

Mundo Louco: Enquanto atirava, pesquisa notícias sobre o crime no Facebook

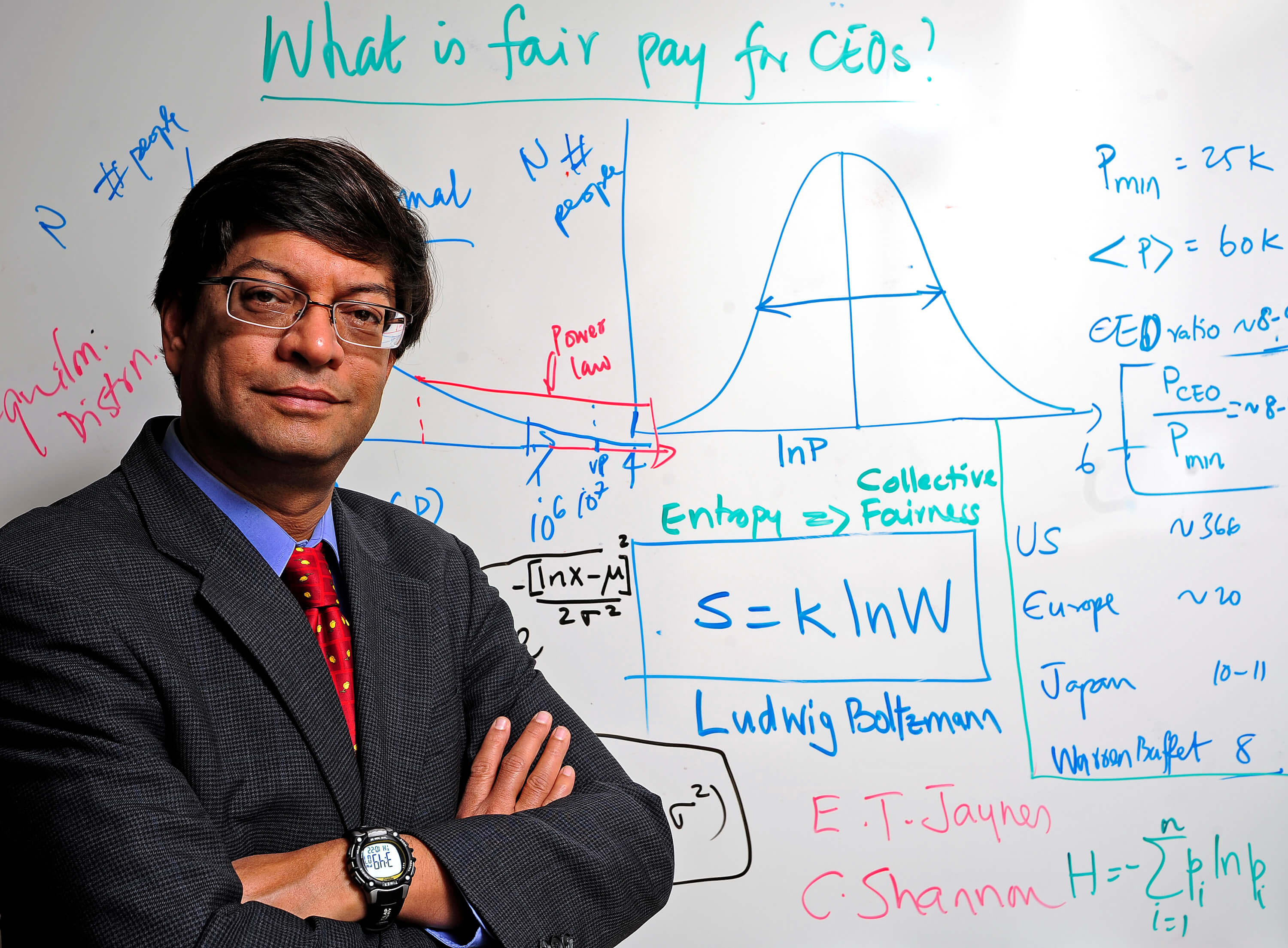

Econofísica x Economia Financeira: similitudes e diferenças

Resumo:

In line with the recent research and debates about econophysics and financial economics, this article discusses on usual misunderstandings between the two disciplines in terms of modelling and basic hypotheses. In the literature devoted to econophysics, the methodology used by financial economists is frequently considered as a top-down approach (starting from a priori “first principles”) while econophysicists rather present themselves as scholars working with a (empirical data prone) bottom-up approach. Although this dualist perspective is very common in the econophysics literature, this paper claims that the distinction is very confusing and does not permit to reveal the essence of the differences between finance and econophysics. The distinction between these two fields is mainly investigated here through the lens of the Efficient Market Hypothesis in order to show that, in substance, econophysics and financial economics tend to have a similar approach implying that the misunderstanding between these two fields at the modelling level can therefore be overstepped.

Fonte: On the "usual" misunderstandings between econophysics and finance: some clarifications on modelling approaches and efficient market hypothesis- Marcel Ausloos, Franck Jovanovic, Christophe Schinckus. 2016

In line with the recent research and debates about econophysics and financial economics, this article discusses on usual misunderstandings between the two disciplines in terms of modelling and basic hypotheses. In the literature devoted to econophysics, the methodology used by financial economists is frequently considered as a top-down approach (starting from a priori “first principles”) while econophysicists rather present themselves as scholars working with a (empirical data prone) bottom-up approach. Although this dualist perspective is very common in the econophysics literature, this paper claims that the distinction is very confusing and does not permit to reveal the essence of the differences between finance and econophysics. The distinction between these two fields is mainly investigated here through the lens of the Efficient Market Hypothesis in order to show that, in substance, econophysics and financial economics tend to have a similar approach implying that the misunderstanding between these two fields at the modelling level can therefore be overstepped.

Fonte: On the "usual" misunderstandings between econophysics and finance: some clarifications on modelling approaches and efficient market hypothesis- Marcel Ausloos, Franck Jovanovic, Christophe Schinckus. 2016

Assinar:

Postagens (Atom)